Before delving into the intricacies of stem cell therapy costs, it is essential to lay the groundwork by exploring the diverse landscape of stem cell treatments available today. Stem cell therapy has emerged as a revolutionary medical field, offering a wide array of potential treatments and applications. By understanding the different types of stem cell therapies and their respective benefits, limitations, and implications, we can gain a comprehensive perspective on the factors that contribute to the overall cost of these groundbreaking treatments.

The Basics of Stem Cell Therapy

To appreciate the costs associated with stem cell therapy, one must first grasp the core principles and mechanisms behind this groundbreaking treatment approach. This section will therefore introduce the essentials: defining stem cells, explaining the process of stem cell therapy, and outlining the various types of stem cell therapies available.

What are stem cells?

Stem cells are the building blocks of life, the foundation from which all tissues in your body are made. They are unique cells with an extraordinary power – the ability to develop into many different types of cells in the body during early life and growth. In addition, in many tissues, they serve as an internal repair system, dividing without limit to replenish other cells.

The two main types of stem cells are embryonic stem cells and adult stem cells. Embryonic stem cells, as the name suggests, come from embryos, while adult stem cells are found in small quantities in most adult tissues, like bone marrow or fat, also called adipose tissue.

How does stem cell therapy work?

Stem cell therapy, also known as regenerative medicine, is a type of treatment that uses stem cells to repair damaged or diseased tissues in the body. It’s like providing a repair kit for the body, encouraging the growth of new, healthy cells to replace diseased ones.

The process usually involves isolating stem cells from a source, which can be the patient’s own body or a donor. Common sources include blood, bone marrow, or adipose tissue (fat). These cells are then processed, if necessary, and subsequently introduced into the patient’s body where the damage or disease exists. Once in the targeted area, these cells have the potential to contribute to regenerating and repairing the tissue.

Different types of stem cell therapies:

- Bone marrow transplant: This is one of the most widely-used forms of stem cell therapy. In this procedure, stem cells are harvested from the bone marrow, then processed and infused back into the same patient (autologous transplant) or into another individual (allogeneic transplant). It’s a common treatment for certain blood cancers, such as leukemia and lymphoma, as well as other blood disorders.

- Cord blood therapies: These therapies use stem cells extracted from the umbilical cord blood after birth. Like bone marrow transplants, cord blood therapies are often used to treat blood disorders such as leukemia. They can be particularly valuable as the stem cells in cord blood are usually more adaptable and are less likely to cause complications compared to stem cells from other sources.

- Regenerative medicine for orthopedic issues: This includes treatments where stem cells are injected into joints to treat conditions such as osteoarthritis or cartilage damage in the knees. These treatments are areas of active research and have shown promise in early trials, but it is important to note that they are not yet widely accepted as standard care and more research is needed to fully understand their efficacy and safety.

Armed with a better understanding of what stem cell therapy is, let’s now explore the various factors that influence its cost.

Factors Influencing the Cost of Stem Cell Therapy

Like any medical procedure, the cost of stem cell therapy can vary significantly. There’s no one-size-fits-all price tag because several factors come into play. Understanding these influencing factors will give you a clearer picture of what you can expect to pay for this type of therapy. Let’s delve into them one by one:

Type of Stem Cell Therapy

The cost of stem cell therapy can vary dramatically depending on the type of therapy. As mentioned earlier, there are numerous stem cell therapies available today, each with different methods of collection, preparation, and administration of the stem cells. For instance, a bone marrow transplant typically costs more than therapies using cord blood because the procedure to collect bone marrow is more complex and time-consuming.

Geographic Location of the Treatment

Geography plays a significant role in the cost of stem cell therapy. In general, the costs are higher in developed countries like the U.S., mainly due to the higher overall cost of healthcare. Conversely, in countries like Mexico and India, the costs can be considerably lower, though this can come with its own set of considerations, like travel expenses and differences in regulatory standards.

Level of Care Needed Before, During, and After Therapy

The complexity of the patient’s condition and the level of care required can significantly impact the total cost of stem cell therapy. Patients who need additional testing or medical procedures before the therapy, or intensive care during and after the therapy, will likely incur higher costs.

Use of Proprietary Technology or Methods

Some clinics and hospitals use proprietary technology or methods for isolating and administering stem cells. This can sometimes result in higher costs due to the unique benefits these technologies offer, such as increased stem cell yield or improved cell viability.

Case Study: Comparison of Costs Based on These Factors

To illustrate these points, consider the example of John and Sarah, both opting for stem cell therapy. John is undergoing a bone marrow transplant in the U.S. for a severe condition, requiring extensive pre and post-treatment care. On the other hand, Sarah is receiving cord blood therapy in India for a less severe condition, with minimal pre and post-treatment care.

While the cost for John, considering the complexity of the procedure, the location, and the level of care needed, might range around $50,000-$200,000, Sarah’s treatment might cost considerably less, say around $10,000-$20,000, due to the lower cost of the procedure and the healthcare cost in the geographic location.

This example is oversimplified but helps illustrate how these factors can contribute to the cost difference in stem cell therapy.

Now that we’ve discussed the influencing factors, let’s delve into the average costs of stem cell therapies.

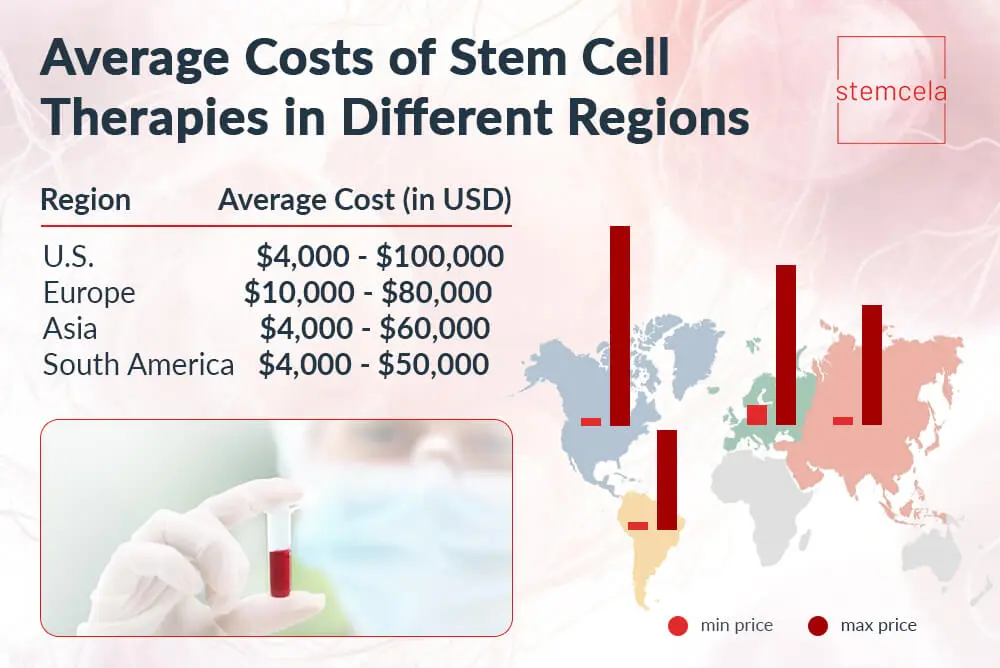

Average Costs of Stem Cell Therapies

As we’ve established, the cost of stem cell therapy varies widely depending on a range of factors. However, to give you an idea of what you might expect to pay, we’ve compiled data showing the average costs of stem cell therapies in various regions around the world.

Average Stem Cell Therapy Cost in Different Regions

Stem cell therapy price prediction

There are several reasons why the costs of stem cell therapies might increase in the future

- Increased Demand: As more people learn about the potential benefits of stem cell therapy, demand has risen, which can drive up prices.

- Technological Advancements: As technology advances, new methods and equipment are introduced that can improve the efficacy and safety of stem cell therapies. However, these advancements often come at a cost, which can be reflected in the price of therapy.

- Regulatory Changes: Changes in healthcare regulations can also impact costs. For example, if a country introduces stricter regulations surrounding stem cell therapy, this could increase costs due to the added requirements for compliance.

- Economic Factors: Broader economic factors can also impact the cost of healthcare, including stem cell therapy. For instance, changes in the economy can affect the price of resources needed for therapy, which can in turn affect the overall cost of treatment.

Understanding these average costs and why they’ve changed over the years can provide a better perspective on the financial aspect of stem cell therapy. Next, we’ll explore the process and additional costs that you may need to consider when planning for this treatment.

The Process and Additional Costs

When considering the total cost of stem cell therapy, it’s crucial to look beyond just the price of the procedure itself. There are multiple stages in the process, each with its own associated costs. Additionally, there might be unexpected expenses that you’ll need to factor into your budget. Let’s break it down:

Pre-treatment Consultation and Tests

Before you can undergo stem cell therapy, your doctor will need to evaluate your condition and suitability for the treatment. This will typically involve a consultation, which may cost anywhere from $100 to $500, depending on the specialist and the location.

In addition, several tests might be needed to gain a comprehensive understanding of your health status. These could include blood tests, imaging studies like MRI or CT scans, and other diagnostic procedures, each ranging from $200 to several thousand dollars based on their complexity and the healthcare market rates in your location.

Cost of the Procedure Itself

This is the primary cost and involves the collection, processing, and administration of the stem cells. As we discussed earlier, these costs can vary greatly based on the type of therapy, the location of treatment, and the use of any proprietary technologies.

Post-treatment Care and Follow-ups

After the therapy, you’ll likely need follow-up appointments to monitor your progress and manage any potential side effects. These appointments might range from $100 to $500 per visit. Also, if additional treatments or medications are required to manage side effects or enhance the effectiveness of the therapy, these will add to the overall cost.

Additional Costs

Finally, don’t forget about the potential additional costs that might not be included in the treatment price. These could include:

- Travel expenses: If you’re traveling out of state or even out of the country for your treatment, you’ll need to account for costs like airfare, car rental, and gas.

- Accommodation: Depending on how far you’re traveling and how long your treatment and recovery will take, you might need to pay for a hotel or other accommodation.

- Meal and miscellaneous expenses: While you’re away from home, you’ll have to pay for meals and any other daily living expenses.

Remember, these costs can add up quickly, so it’s important to consider them when budgeting for your stem cell therapy. Having a comprehensive understanding of all potential costs can help you avoid unexpected surprises and ensure a smoother, less stressful treatment journey.

Next, we’ll delve into one of the major questions in the financial aspect of stem cell therapy – How does insurance come into play?

Insurance and Stem Cell Therapy

In an ideal world, insurance would cover any treatment needed to maintain or improve one’s health. Unfortunately, the reality is often more complicated, especially when it comes to cutting-edge treatments like stem cell therapy. Let’s delve into how insurance companies view stem cell therapy, what extent of coverage you might expect, and gain some insights from an insurance provider.

How Insurance Companies View Stem Cell Therapy

Most insurance companies categorize treatments into two main types: experimental and standard-of-care. Standard-of-care treatments are those that are widely accepted by the medical community as effective and reliable. Experimental treatments, on the other hand, are newer and still being studied for their efficacy and safety.

Given the novelty and the ongoing research surrounding stem cell therapy, many insurers still consider it experimental, with the exception of certain procedures like bone marrow transplants for specific conditions. This distinction is crucial because many insurance policies do not cover treatments that are deemed experimental.

Extent of Coverage for Different Types of Therapies

When it comes to stem cell therapies, coverage varies widely based on the type of therapy and the specifics of your insurance plan. Some insurance companies may cover part or all of the cost of certain stem cell therapies if they’re considered a standard-of-care treatment.

For instance, a bone marrow transplant for a condition like leukemia is likely to be covered by many insurance companies, as this is a widely accepted use of stem cell therapy. However, using stem cells to treat conditions like arthritis or heart disease may not be covered because these uses are still considered experimental by many insurers.

Expert Interview: Insights from an Insurance Provider

“Insurance coverage for stem cell therapies is a rapidly evolving field,” explains Jane Paul, an insurance expert with over two decades of experience. “As more research is conducted and these therapies become more mainstream, we anticipate a shift in coverage policies. However, patients should always consult their individual insurance provider for the most accurate information. There can be a great deal of variation between different plans and companies.”

The insurance landscape for stem cell therapy is complex and can feel overwhelming. But remember, it’s crucial to have these discussions with your insurance provider and healthcare professionals. This will help you to get a clear understanding of what’s covered, what’s not, and what you’ll need to budget for out-of-pocket.

Finally, we’ll explore the future of stem cell therapy costs and some financing options available to patients.

Future Predictions and Trends

Predicting the future of healthcare costs, especially in a rapidly evolving field like stem cell therapy, can be a challenge. However, certain trends can give us insight into how costs might change over time. Let’s explore how technology, research, and insurance coverage might influence the future costs of stem cell therapy.

Impact of Technology and Research on Future Costs

Technological advancements and ongoing research play a significant role in shaping the future of stem cell therapy costs. As new methods and technologies emerge, they have the potential to make procedures more efficient and safer. In turn, this could lead to lower costs.

For example, advances in lab-grown stem cells could eventually eliminate the need for donor cells for certain therapies, potentially reducing costs. Likewise, improved techniques for isolating and administering stem cells could make the procedure quicker and less invasive, further driving down costs.

However, it’s also important to note that new technologies often come with high initial price tags, which could temporarily increase costs.

Possible Changes in Insurance Coverage

As stem cell therapies become more mainstream and additional data supports their efficacy and safety, it’s likely that insurance companies will expand their coverage for these treatments. This change could make stem cell therapy more accessible and affordable for a larger number of patients.

Expert Opinion: Predictions from a stem cell specialist

According to genetics and stem cell specialist Vyacheslav Klymenko, – “The future of stem cell therapy costs is tied to a delicate balance between innovation and accessibility. On one hand, as we continue to refine and improve these therapies, initial costs may increase due to the investments needed for research and development. On the other hand, as these treatments become more common and standardized, economies of scale could bring costs down. In the long term, I predict a gradual decrease in costs as technology improves, regulations adapt, and market competition intensifies.”

While it’s hard to predict with certainty, understanding these potential trends and factors can provide some insight into the future of stem cell therapy costs.

Conclusion

Navigating the costs of stem cell therapy can be a complex journey. In this guide, we’ve explored the various factors that influence these costs, from the type and location of the therapy to additional expenses that might come into play. We’ve discussed how insurance companies view stem cell therapy and how coverage can vary greatly depending on the specific therapy and insurance policy.

We’ve also looked at potential future trends, including the impact of technology and research on costs and possible changes in insurance coverage. While predicting future costs comes with its challenges, understanding these trends can provide some insight into what to expect down the line.

But remember, while the costs are a significant aspect, they’re just one part of the bigger picture. It’s equally important to consider the potential benefits, risks, and alternatives of stem cell therapy. As with any healthcare decision, it’s crucial to do thorough research, consult with healthcare professionals, and weigh all your options.

At the end of the day, the goal is to make an informed decision that supports your health and well-being. While the world of stem cell therapy can seem overwhelming, understanding the associated costs is a significant step towards making that informed decision. So take this knowledge, empower yourself, and move forward confidently on your healthcare journey.

That’s all for now. If you found this guide helpful, don’t forget to share it with others who might benefit. Stay tuned for more insights and guides on stem cell therapy.

Frequently Asked Questions

Stem cell therapy is a complex procedure that involves a lot of expertise, technology, and resources. From harvesting the stem cells to processing them and finally administering them, each step of the process contributes to the cost. Moreover, if proprietary technologies are used, it can add to the cost. Additionally, the post-treatment care and possible additional costs like travel, accommodation, and meals can also make it expensive.

Currently, many insurance companies consider certain types of stem cell therapies to be experimental and do not cover them. However, there are exceptions, like bone marrow transplants for specific conditions, which may be covered. It’s always best to check with your individual insurance provider to understand what is and isn’t covered under your specific plan.

Yes, many clinics offer financing options for stem cell therapy. Some companies also specialize in providing medical loans or payment plans. However, like any financing decision, it’s important to understand the terms and conditions before making a commitment.

The cost of stem cell therapy can vary greatly depending on the country. Generally, costs can be lower in countries like those in South America and Asia compared to the U.S. and Europe. However, it’s important to consider other factors such as the quality of care and potential additional costs when looking at treatment abroad.

When budgeting for stem cell therapy, it’s important to consider not only the cost of the procedure itself but also the costs associated with pre-treatment consultation and tests, post-treatment care, and any potential additional costs like travel, accommodation, and meals. Always ask your healthcare provider for a detailed breakdown of costs to avoid any surprises.

No, stem cell therapy and PRP therapy are not the same, though they are both types of regenerative medicine. To learn more about the differences check the following post – ‘PRP vs Stem Cell Therapy. All you need to know.’